If you have ever heard of the Alternative Minimum Tax (AMT), you know it has been a major issue for decades. Many taxpayers found themselves paying a substantial alternative minimum tax, despite legitimate deductions that would ordinarily subject them to lower income tax rates. In this post, we’ll provide a little background on the AMT, and discuss how the rules have changed under the recent tax reform.

In our last post, we discussed deductions under the Tax Cuts and Jobs Act (“TCJA”). While giving us lower income tax rates, the TCJA also eliminated (or limited) many of the personal itemized deductions and exemptions to which we had become accustomed.

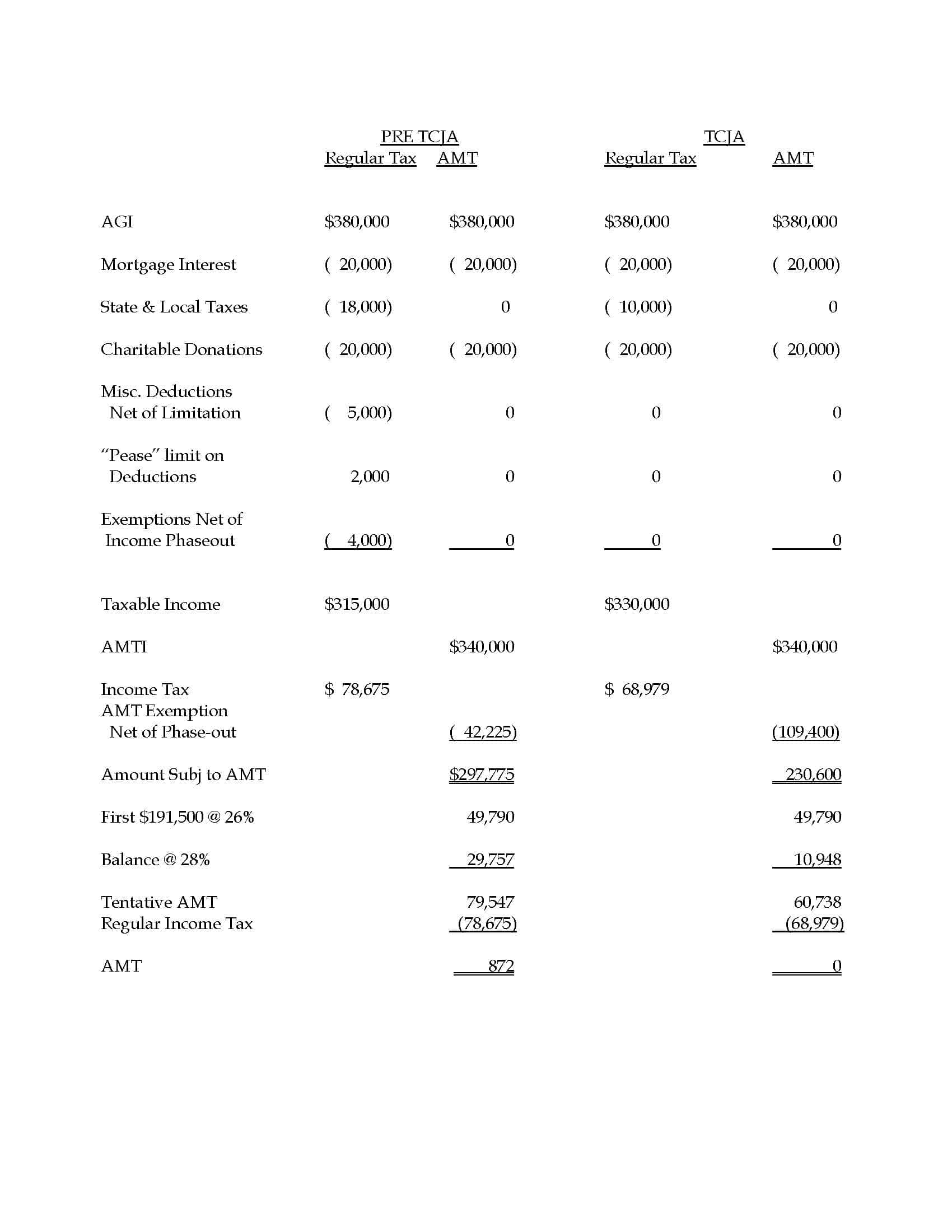

We used a fictional married couple (filing jointly) with no children or other dependents to compare the “regular” income tax they would face in 2018 under TCJA with the same tax without the TCJA. For our comparison, the couple had salaries and other investment income (no qualifying business income; a subject for a later discussion) resulting in Adjusted Gross Income (“AGI”) of $350,000. In this example the elimination or reduction of certain itemized deductions produced a higher taxable income; however, coupling higher taxable income with lower tax rates resulted in lower “regular” income taxes for this couple.

So why the quotes around the word “regular” income tax? For years before the TCJA, we operated under a parallel system of taxation intended to ensure that some taxpayers with certain levels of income and specified deductions paid at least a certain amount of tax. This tax was the Alternative Minimum Tax (“AMT”) and calculation of this tax essentially required the taxpayer to make two calculations under the “regular” rules for income tax and for the AMT. The AMT net, under prior law, had grown to capture many taxpayers.

While the AMT, under prior law, provided an exemption for married couples of $86,200, it began to phase-out once alternative minimum taxable income (“AMTI”) exceeded $164,100, and was completely eliminated when AMTI reached $508,900. To make matters worse for taxpayers, the AMTI calculation eliminated a handful of itemized deductions, including state and local taxes. This created an AMTI higher than one’s “regular” taxable income. So, many taxpayers subject to AMT under prior law were already losing deductions that are now eliminated, or limited under TCJA. The law prior to TCJA taxed this higher AMTI (with its fewer deductions) at rates of 26 and 28% on non-capital gains.

Although TCJA eliminated the AMT for corporations, it retained AMT for individuals and other non-corporate taxpayers. However, the changes under TCJA affecting the AMT rules did substantially decrease the number of taxpayers that will come within its reach. For example, a married couple now would receive an AMT exemption in 2018 of $109,400, and that exemption would not begin a phase-out until AMTI exceeded $1 million. Looking at our fictional married couple, we can see both the “regular” and AMT calculations to them in 2018 without and with the changes of the TCJA. Under this scenario, our hypothetical couple would not be subject to AMT, but instead, would pay on “regular” taxable income.

As you can see above, the AMT for the couple would have added another $872 for a total income tax tab of $79,547 in 2018 without the changes of the TCJA. Under the TCJA, the couple would have income taxes of $68,979 with no additional AMT due to the increased AMT exemption and the higher threshold before the phase-out of that exemption.

In my next post, I want to review how the TCJA attempted to equalize the income tax for the non-corporate taxpayers’ business income with the substantially reduced corporate income tax rate of 21% by the creation of the Qualified Business Income Deduction.